7 Strategic Decisions that could put Uber back on the highway

Uber finally has a new CEO. From all accounts, it appears that the reins of the company are falling into a solid pair of hands. Dara…

Uber finally has a new CEO. From all accounts, it appears that the reins of the company are falling into a solid pair of hands. Dara Khosrowshahi has his hands full as he starts work. The overall to-do list for Dara and his team will be long and wide-ranging, from rebuilding Uber’s organization at the senior level to fixing/morphing the company’s allegedly toxic culture, boosting employee morale, and dealing with legal battles.

However, the focus of this post is strategy. Dara will need to take several strategic decisions almost immediately to get the company back on track as the most valuable tech company created in the current business cycle. It is no secret that despite the relatively strong financials the company recently posted, it risks losing precious momentum and market share, even as it continues to have an annualized EBIT loss north of $2.5B.

Dara has indicated that a potential IPO is 18–36 months out. This would necessitate a significant change in trajectory and focus for the company. Uber 1.0 (let’s call it that) has multiple large, high-growth businesses. Yet, the company faces questions around unit economics, sliding market share in its core market, potential regulatory risk and threat of disruption from autonomous vehicles. Moreover, the company has gone through a significant recent diminution of public perception. Uber 1.0, while a business of incredible scale and growth, was no longer on the right course towards a successful IPO in the near term.

Uber operates in massive, highly competitive markets globally, and will need to pick its battles to be able to fight them well. Modern technology behemoths that Uber might want to emulate in terms of market position and scale — i.e. Google, Amazon and Facebook — all had a solid, profitable, extensible core market that they had clearly “won” before they ventured into other businesses.

Having a new CEO and new management team members will offer Uber the opportunity to re-valuate many fundamentals of its strategy and begin to build Uber 2.0.

Here is my list of top 7 strategic decisions for Dara:

1. How hard and deep to play in the Autonomous Vehicle space? If there is one strategic decision that will determine how favorably history views Dara’s tenure at Uber, then this would be the one. Over the past two years, Uber visibly made it its highest priority to chase pole position in building Autonomous Vehicles (AVs) — perhaps at any cost.

Dara needs to decide how much he wants to prioritize AV development, and re-evaluate what approach (build/partner/buy) he wants to take for each subsystem that goes into bringing AVs to market.

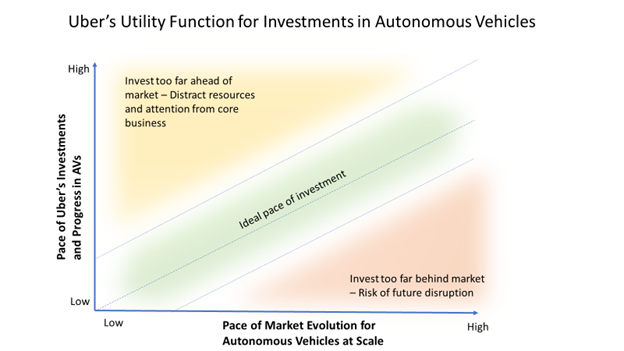

It is extremely important for Uber to get the timing of its investments and strategy in this space right. Investing too far ahead of the market would mean diverting resources and focus away from the core ride-sharing and personal transportation business. On the other hand, falling behind the market would bring the risk of other AV leaders building out a network of vehicle supply and demand to parallel Uber’s. The picture below illustrates this dynamic.

How many years away we are from full level 5 (or even level 4) AVs at scale will drive the nature of Uber’s AV strategy. If fully autonomous driving at scale is 2 years away (as Elon Musk has promised), then Dara needs to continue to bet the company on AV development, and be prepared to build the core autonomous software, HD mapping and whatever other components it needs to in order to get there in the target time-frame. Potential partners may not have the same sense of urgency, and the partnering overhead will slow things down.

However, if full autonomous driving in unconstrained environments is further away as many pragmatists are beginning to realize, then a more partner-centric ecosystem approach will make more sense.

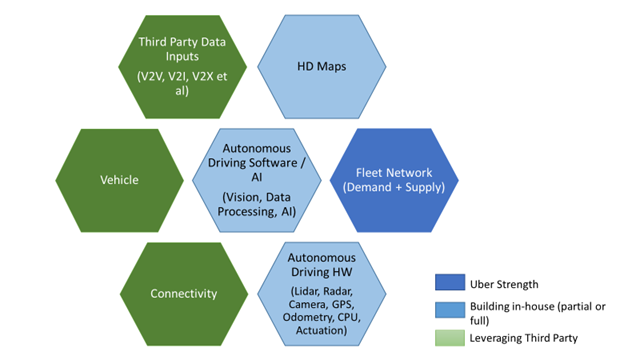

The figure below shows at a high level the various technological components involved in building AV systems, and where Uber is currently known to play.

By partnering more deeply with a small number of forward-thinking OEMs, for instance, Uber can decrease the resource intensity of the effort, leverage existing bodies of knowledge on nuts-and-bolts automotive technologies, and possibly build a more lasting, de-risked solution. Pre-existing expertise in core automotive areas could be important to getting AVs to mass scale production. As another example, a player such as Uber may not need to spend hundreds of millions (or billions) of dollars a year to build and maintain full HD maps in-house. It could choose to leverage HD maps from a qualified third party, and build a proprietary real-time data layer on top. Lyft — with announced partnerships with both Waymo (arguably the player furthest ahead in the AV space) and General Motors — has a more concerted partnering strategy by most accounts.

I believe network players such as Uber and Lyft are well positioned to benefit from the AV space, and the market dynamics provide them breathing room to build out their AV approach and partner ecosystem in a thoughtful manner. Here are some reasons:

- Vehicle Networks and Fleets will be best positioned to commercialize AVs as they can leverage the benefits of vehicle sharing and higher utilization. Given their network’s criticality in deriving the key economic benefit from AVs (i.e. lower cost transportation), network players such as Uber and Lyft will be well positioned to attract partners who develop AV systems before or better than them

- AVs, once rolled out, will likely require a human inside the car for a long time to come (to take care of corner cases, address emergencies, or to meet regulatory requirements). Uber and Lyft — which already have large networks of vehicles with drivers — are positioned well here

- AVs will initially be rolled out in low complexity environments such as highways and spread to denser urban areas over time. Uber’s rideshare business is largely intra-city, which leans towards more complex urban street environments.

- It is possible that by the time AVs do go mainstream, owning the full software stack is not necessary due to sufficient progress of open source initiatives, or wide third-party availability of the technology — similar to what we have begun to see in the broader AI space. Value may move back to the data and the networks, where Uber and Lyft are well positioned

- Regulatory and infrastructure support typically moves at a different pace than technological innovation. While some markets may be quick to build the legal and physical infrastructure required for AVs, the wider market may take much longer

- Most massive technological transitions that involve many types of participants happen over long periods of time. The Cloud space, representing a shift from owned asset (servers on premise) to a third party managed service, provides a good analog for the Transportation-as-a-Service space. Clouds services are well over ten years in, and while adoption has grown aggressively, penetration is still relatively early, providing a long runway. The transition to AVs is likely to be similarly spread over several years if not decades

In summary — while getting the AV timing and strategy right is absolutely critical to Uber, the good news is that the company may have breathing room to build a more thoughtful approach to getting AVs to the market. And this approach could be more ecosystem-centric, leveraging third parties — similar to what Android/iOS did in mobile and Windows did in the desktop space

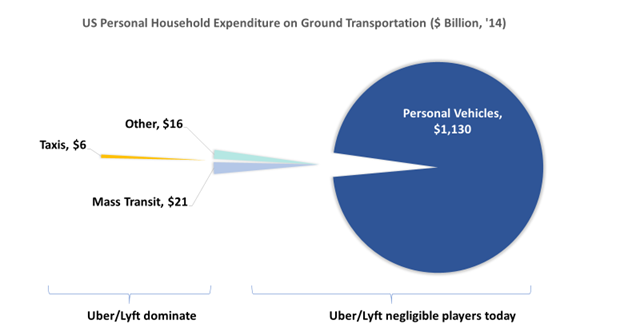

2. How to build a real Transportation-as-a-Service business? Uber and Lyft have outgrown the pre-existing taxi market in their core geographies, but are barely beginning to scratch the surface of a much larger market — that of personal vehicle replacement. The figure below illustrates the relative sizes of consumer spend on each of these buckets. Business spend in these categories is separate, but this captures the basic idea.

Consumers in the US spend over $1.1 Trillion on owning, fueling and maintaining personal vehicles. US auto sales continue to be at record highs year over year. Uber, even with its current annualized gross ride value of over $32B (global number; US likely $15–20B), hasn’t begun to replace personal vehicle ownership at any meaningful scale yet. This is because Uber hasn’t made a dent on the primary use case for personal vehicles — the work commute.

Uber’s on-demand services provide high flexibility and custom routing, but are too costly (and this includes Uber Pool) for the commute use case for most consumers. The commute use case requires a solution that is lower cost, and more predictable and reliable.

The holy grail in the smart transportation business is to address the commute use case more effectively. The broader opportunity is to offer Transportation-as-a-Service (TaaS) subscriptions. Imagine if you could pay a fixed fee — similar to your current car payment — and get reliable transportation between home and work (across modes of transport), along with a number of weekend rides every month.

This would be like Amazon Prime for transportation, except with an ARPU that is an order of magnitude higher. The company that cracks this could have the basis for building a trillion-dollar value business over the years. Uber has trialed offerings along these lines inside major city downtowns, but I believe it’s core model of dedicated car and driver on demand cannot support the price points necessary to serve the commute use case in North America, where most commuters live in the suburbs.

Autonomous Vehicles are not the only path to TaaS. To get to the TaaS vision before AVs are ready to go mainstream, one could look at ideas such as fixed route offerings that pool users along pre-defined routes and times (augmenting public transport); integrating modes of transport beyond cars (e.g. trains, buses, bikes, scooters, EVs); true ride “sharing” (car pool amongst passengers headed in the same direction, rather than paying for a professional driver), or options where the consumer drives the car herself (given that the biggest cost bucket for an Uber ride is the fee for the driver’s labor). There are many startups and larger companies innovating in these segments already, and companies such as Uber can partner/invest/acquire in these spaces, and leverage their scale, brand, user base and balance sheet to get these solutions to requisite scale

3. Growth or profitability? or both? Uber 1.0 appeared to prioritize current and future growth well above profitability. Dara needs to decide where he wants to be on the growth to profitability dial now and in a couple of years. In my view, in the near future, the business would need to demonstrate sustainable profitability in its core segment (i.e. ride sharing in Western markets) while demonstrating a few curated, credible seeds of future growth. Contrary to some recent reporting on the topic, I believe ridesharing as a business can be reasonably profitable in Western markets, and Uber already has the scale to get there. The path to regional profitability doesn’t necessarily involve raising headline prices for consumers. Instead, Uber needs to drive up its net revenue per ride (after discounts, driver bonuses) and effective utilization of vehicles on its network; increase density of UberPool rides (or tweak its business model); and judiciously optimize fixed costs. It appears there is much foundational work on strategic finance and real time reporting that may need to be done, and Dara and whoever he hires as CFO may need to first put in place the right decision support infrastructure that can enable the company to make decisions based on fully loaded costs

4. Transportation or Logistics? or both? Logistics is a very large market adjacent to Uber’s core Transportation market, yet distinct from it. Uber currently has initiatives such as UberEverything (including UberEats for Food Delivery, UberRush for delivering goods) and UberFreight (load pooling for trucks) in the logistics space. It has also previously experimented with other models within on-demand logistics. Uber needs to decide how core Logistics is to its long-term plans. Each of these segments have different industry dynamics, many have a different set of supply or demand partners, and some involve building an entirely new network with a new category of vehicle. Moreover, each segment is highly competitive, with dedicated startups and incumbents fighting to win each of those segments. Are these services really core to Uber’s long term plans, and if so, in what geographies? For the ones that are, the company needs a better plan — organic or inorganic — to win in these spaces. For segments determined to be non-core, it needs to quickly re-deploy teams, capital and attention into its core Transportation business

5. Which geographies? Another decision Dara must make is which international markets Uber wants to “own” over the longer term — and then go all-out after those, while exiting others which don’t move the needle in the right direction. Fortunately, Dara and his team have solid reference points in the Didi (China) and Yandex (Russia) transactions. Markets such as India and Southeast Asia may offer potential long term upside, but will be relatively small, distracting and cash-draining in the near term. Moreover, markets such as India have low ASPs in the ridesharing space with extremely challenging unit economics, and winning such markets sustainably will require very different strategy and tactics than in core Western markets. Are these battles ones that Uber wants to fight and continue investing behind? Or is it better off holding stakes in the market leaders in most emerging markets?

6. How nice to play with regulators? This is one of the stickier decisions. Uber famously grew while disregarding regulations and regulators. This approach worked well for the company in many markets, while it backfired in several others. As a company now at a different stage of evolution, and under new management, Uber has an opportunity to consider a different tack. Dara needs to decide whether to continue with status quo or take a more conciliatory approach towards regulators and town planners. The latter approach could mean slower growth in several markets in the near term, but it could lead to a de-risked regulatory future that public market investors would be more comfortable with. Moreover, such an approach would be more likely to open paths to other models within the broader Transportation-as-a-Service vision.

7. Secure deep-pocketed investor? Softbank Vision Fund’s size and approach enable it to tilt the outcome in leadership battles for massive markets. With Softbank’s interest in owning the ride-sharing space globally, having Softbank on Uber’s side rather than its opponents’ has to be a key strategic step Dara is considering.

(Anupam has been associated with over a dozen startup and growth-stage companies across various sectors and geographies. He brings the perspective of having invested in and partnered with several category-defining marketplaces globally, and a keen interest in strategic finance for growth companies. He can be reached via Linkedin or Twitter.

All data in this post is based on public sources. The author has no visibility into Uber’s current internal strategy or private information. The post reflects the author’s personal views, not those of his employer or affiliates)