Frontier AI labs are rushing to go public. They shouldn't yet

Exploding inference demand does not guarantee predictable revenue or durable margins. The frontier AI labs are extraordinary companies. They may be stronger by listing after better predictability arrives.

The frontier AI labs are extraordinary companies, perhaps among the most important of our era, working at the leading edge of what could be the largest technological transition in our lifetimes, possibly including the path to AGI.

They are also navigating the most rapidly evolving business landscape in modern tech history. Revenue trajectories and margin structures are volatile, and market leadership positions shift on the timescale of weeks. The assumption that the exploding inference demand will translate cleanly into exploding lab revenue and margins is more fragile longer term than the consensus suggests.

As an investor, I spend my time studying where Enterprise AI value actually accrues, drawing on signals from founders and enterprise operators deploying AI into real workflows. I have also invested in several companies that later went public. Public markets can be a powerful launching pad once a business is ready. But if a company arrives too early, they can narrow its mission, distort its priorities, or even maim it.

The question worth asking is narrower than the bull-vs-bear debate. It is not whether the labs are important. They obviously are. It is whether listing publicly at this specific moment, before their revenue model, margin profile, and market-share dynamics stabilize, makes them stronger companies for the long journey ahead.

My view: a public listing now would impose premature constraints and increase the risk that these companies fall short of their own ambitions. Hockey-stick growth and euphoric demand may well allow strong IPOs in the current window.

The question to ask is whether listing now helps the labs become the companies they aim to become.

Why the IPO rush

The advice to go public now is not irrational. The window is open and investor demand is euphoric. Capital requirements are enormous and climbing. Employees want liquidity, existing investors want DPI, and public stock becomes liquid acquisition currency. The larger a private valuation grows, the harder it becomes to stay private without public market validation. And the first AI lab IPO may define the category for everyone who follows.

But none of this speaks to whether the company is fundamentally stronger once it goes public. The advisory ecosystem around a generational company runs on shorter-duration incentives than the company itself. The founders, management, and long term investors should ask whether the event makes the company stronger five or ten years from now.

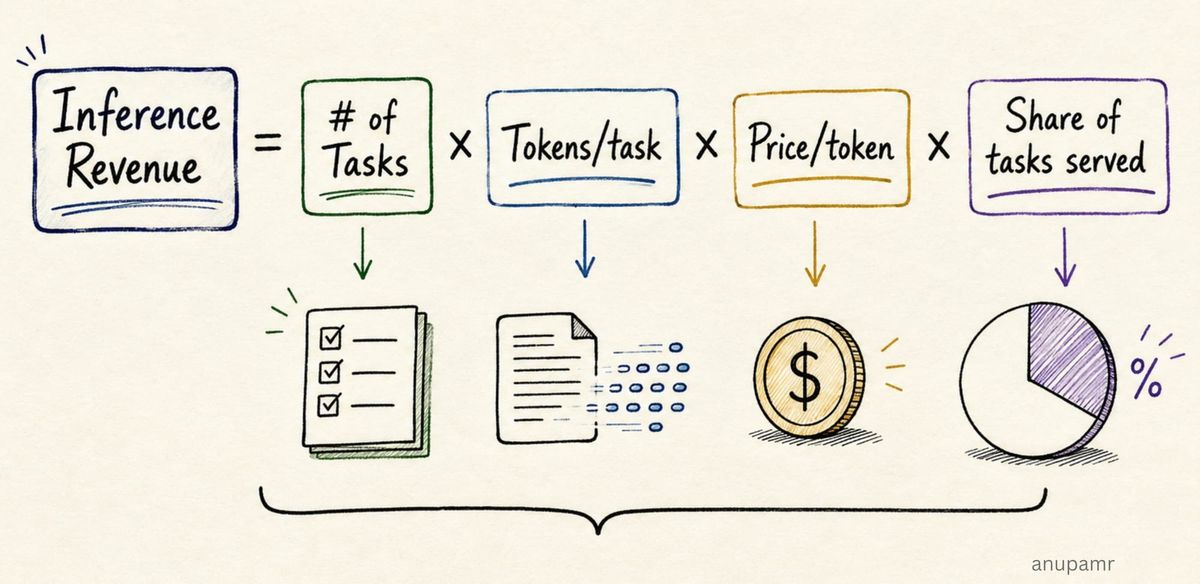

The inference revenue equation

Foundation labs are showing some of the fastest revenue growth in history at their scale. Inference is the engine driving explosive revenue growth. And the inference volume underneath is set to keep rising exponentially as workflows move to native AI usage.

So frontier inference revenue will continue smoothly up the exponential curve, right?

Let’s take a look. Deconstruct a model API's revenue line today and you get something close to the following:

Overall task volume will likely continue to rise sharply as AI becomes embedded in enterprise workflows, agents, and programmatic systems.

However, every other term on the right is under sustained pressure from tech advancements and intense competition.

Tokens per task are falling for any given task. Smaller models, better retrieval, caching, tighter agents, and less context bloat all push in the same direction. The industry spent the last two years discovering how much it could do with fewer tokens, and that work compounds.

Price per token is under relentless pressure at any given capability level. Competition and open weights have opened pricing gaps of more than 20x against best-in-class proprietary models for many tasks. To defend pricing power, frontier labs need a meaningfully better model in market every few months.

Share of tasks served by frontier models is likely to leak over time. The leading indicators all point to falling market share for frontier models in programmatic use. In my experience, builders often start with the best model available when attacking a new problem. But once the workflow automation stabilizes, they optimize: routing work to smaller models, open-weight models, local inference, and customer-hosted systems. The default path trends toward the cheapest model that clears the bar. Frontier models will remain worth paying for on the hardest tasks, but those may represent only a fraction of total volume.

Some of the smartest people in the tech world are working on optimizing inference intensity per unit of work, including many at the frontier labs themselves. Their work compounds, multiplicatively, against the volume term.

In recent months, inference volume growth has overwhelmingly outrun the downward pressures, producing superlative revenue growth for frontier models. Anthropic has scaled from ~$9B to a reported $47B+ run-rate in months as enterprise LLM usage hit its first major S-curve, with agentic workflows, coding harnesses, and token maxing all driving usage up.

The equation still holds. These gains are happening while tokens/task, price/token, and flow share are all under pressure. The question is where volume growth nets out against the other three terms once routing, caching, distillation, and open-weight competition mature, and budgets tighten.

Run the arithmetic forward. Assume inference volume grows 10x in a year (aggressive off a large base, but plausible). Suppose over the same period, tokens per task fall 3x, price per token falls 5x, and the model’s share of tasks halves. Illustrative assumptions, none is directionally outside the range of forces already visible in the market.

Multiply it out: 10 / (3 × 5 × 2) ≈ 0.33x.

A tenfold rise in inference volume could produce a 67% drop in revenue from that stream for a frontier model in this example.

Different assumptions could flip the result. A model that gains task share, gets used for more complex tasks, or ships a more advanced version with real pricing power could see the same equation net to 3x growth instead.

The structural point is that LLM API revenue is in a period of low predictability and lumpy growth. Public markets have severe disdain for both.

What about the labs' extraordinary enterprise NRR numbers that have been reported? Strong NRR over short periods can simply reflect a fast-adoption wave, not necessarily product stickiness. When the underlying product is interchangeable, customers expand spending while they're enthusiastic and can switch to another product when a better one arrives. NRR can look strong right up until it doesn't.

The labs earn from multiple streams in addition to raw inference API revenue: consumer subscriptions, enterprise contracts, and product surfaces like Claude Code and Codex. However, inference is the engine the market expects to drive explosive near-term growth. And a significant part of inference growth will come from business usage, which we focus the rest of this writing on.

The labs may absolutely climb into more durable layers. The question is whether they should do that under public-market scrutiny or in private.

The frontier model may become the exception, not the default

In my conversations with our CXO community and enterprise operators, the primary model family and coding harness of choice rotates every few months as users experiment and new capabilities ship. No frontier model has held mindshare long enough to deeply anchor anyone's stack yet.

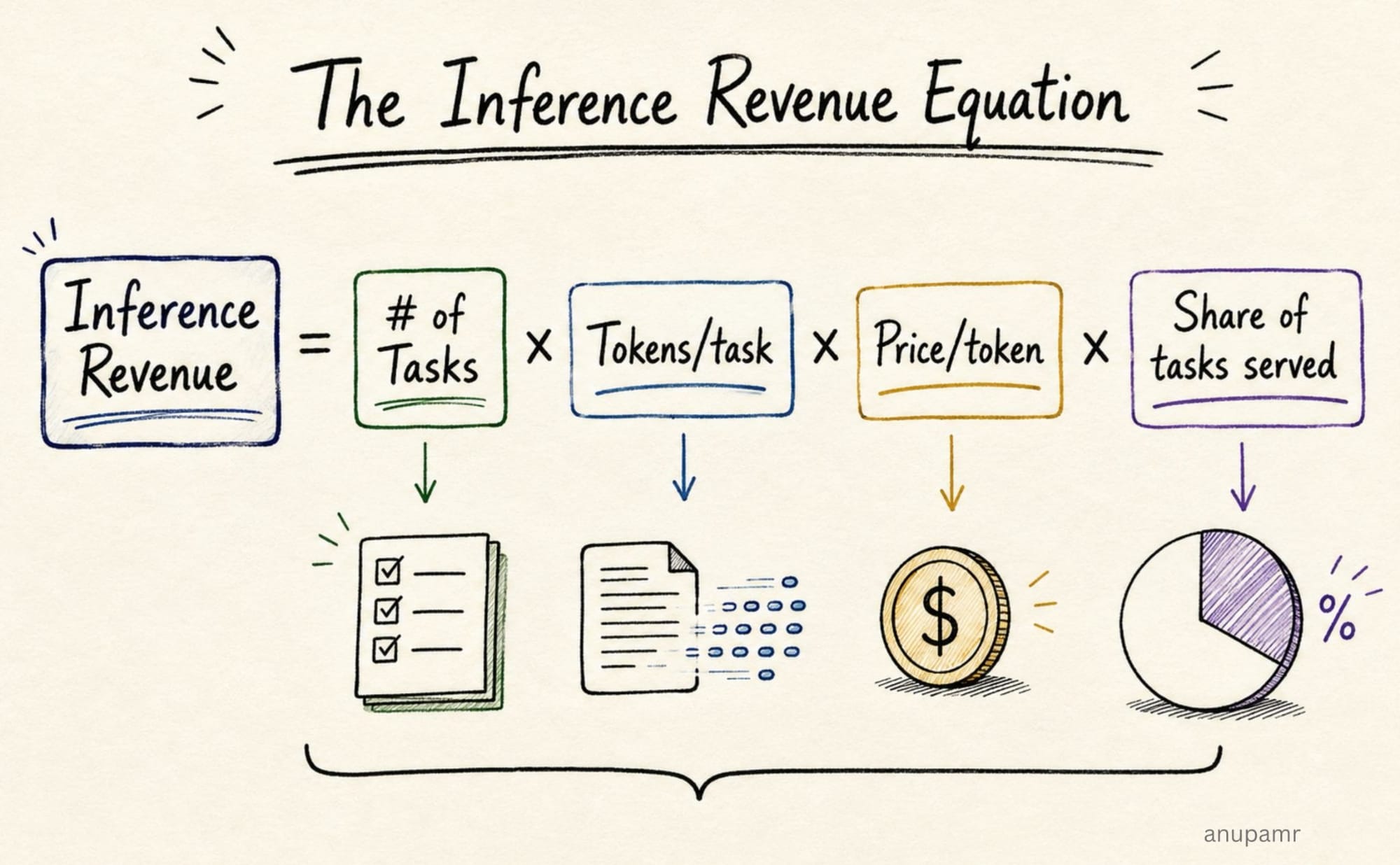

Here is a key part the inference demand-curve optimism misses. Most enterprise workflows do not need the best model at every step. They need a reliable-enough model wrapped in guardrails, retrieval, evals, structured outputs, deterministic tools, and human escalation. The intelligence lives in the system, not in any single call.

In healthcare, legal, text classification, and a rapidly growing list of domains, small specialized models already beat large horizontal ones on the specific task, at a fraction of the cost, with easier adaptation. Once it is established that small, open, or local is good enough for a task, the frontier model stops being the default for it and becomes the exception path reserved for the heaviest lifts.

Using the latest frontier model for routine work is like using a bazooka to swat a fly. You waste the bazooka, and you may still miss the fly. A purpose-built swatter does the job better.

Enterprise AI increasingly revolves around routing and orchestration. The smartest founders I work with have built model routers into their agentic systems for years, precisely to operate that hierarchy. Everyone else is catching on and routing is on its way to becoming standard infrastructure for programmatic use of models. Some steps need frontier reasoning. Many steps need classification, summarization, transformation, validation, or tool use.

Once the task at hand is known, the question becomes: what is the cheapest model that clears the bar?

Once that routing layer becomes standard infrastructure, frontier API usage growth may decouple from total AI usage growth, because the router is designed to keep the expensive model out of the loop wherever a cheaper, faster or local one suffices. The frontier model of the day may end up owning the hardest few percent of problems.

What else the public markets will put under scrutiny

Public capital eventually demands a predictable, profitable business model, and the act of going public forces several uncomfortable things under a continuous scanner.

Margin structure and its quarterly trajectory becomes legible. Right now the private market is largely chasing high-growth AI revenue and forgiving on the gross margin structure. The public market tends to be more discerning over time. An 80 percent gross margin stream and a 30 percent gross margin stream deserve very different multiples.

Foundation lab margins sit on top of subjective assumptions about training cost allocation, capacity commitments, capex depreciation schedules, costs of supporting free users, and inference optimization. As a private company you can leave those assumptions soft, and focus on optimizing them later. A public company will be asked to show the real margin structure, line by line, every ninety days.

Margin consistency over time is key. Going from 30% gross margin one quarter to 50% the next to 40% the quarter after can be acceptable in private markets, but is devastating in public ones. I have seen this up close.

The circular AI infrastructure economy. A meaningful slice of the AI infra-foundation boom runs on commitments that loop back on themselves, often between the same names in different seats. Labs commit hundreds of billions to compute based on anticipated demand and compute efficiency assumptions. Cloud providers, component vendors, and chipmakers book those commitments as demand. Many of those same parties are also large equity investors in the labs, and investment dollars flow back as revenue.

The loop can muddy the true cost of the infra, potentially decoupling demand from true cost. That demand and those commitments then strain fixed capacity. Components clear at scarcity prices, with memory and GPU prices rising several-fold on the strength of forward orders.

This holds together as long as the demand assumptions underneath the commitments at each major link of the chain keep being validated. If they are not, the loop may unwind with a domino effect into the classic infrastructure boom-and-bust that goes well beyond the labs.

The current buildout has trillions resting on assumptions about future inference demand, future model revenue, and future compute intensity. If those assumptions reset, the shock reverberates through cloud contracts, data centers, power, memory, GPUs, and the private credit financing much of the buildout.

Public market scrutiny risks precipitating this. A private company can work through these as its business model and the AI ecosystem mature. A public company has to disclose the obligations, defend the margins, and re-explain the story every quarter, potentially forcing the system to confront its own assumptions before the structure has stabilized.

Public-market momentum is self-reinforcing in both directions

A rising public stock is its own asset. It tightens recruiting, opens enterprise doors that were closed, expands acquisition currency, and lowers the cost of every subsequent capital raise.

A listing also rewires the operating environment in ways management teams often underweight. Public markets are a daily referendum where every missed release, competitor benchmark, margin question, and executive departure becomes part of a running narrative. A major drawdown puts talent packages underwater and enterprise buyers ask the procurement questions that quietly kill deals. These dynamics feed each other: a price reset triggers talent loss, which triggers execution slip, which triggers the next reset.

A private company can say it is working on evolving its revenue mix, margin structure, and long-term position in the stack. A trillion-dollar public company cannot. Public investors may tolerate losses, heavy capex, and aggressive growth spending when the long-term model is legible. What they punish brutally is unpredictability, which is precisely the dimension on which the labs must remain most fluid in order to achieve bigger goals.

The labs are entering a period of intense business model evolution: climbing into more durable layers, developing new revenue streams and potentially growing into enterprise solutions companies. This work requires a forgiving operating environment that can avoid the negative self-reinforcing spiral.

A history lesson on value capture vs volume growth

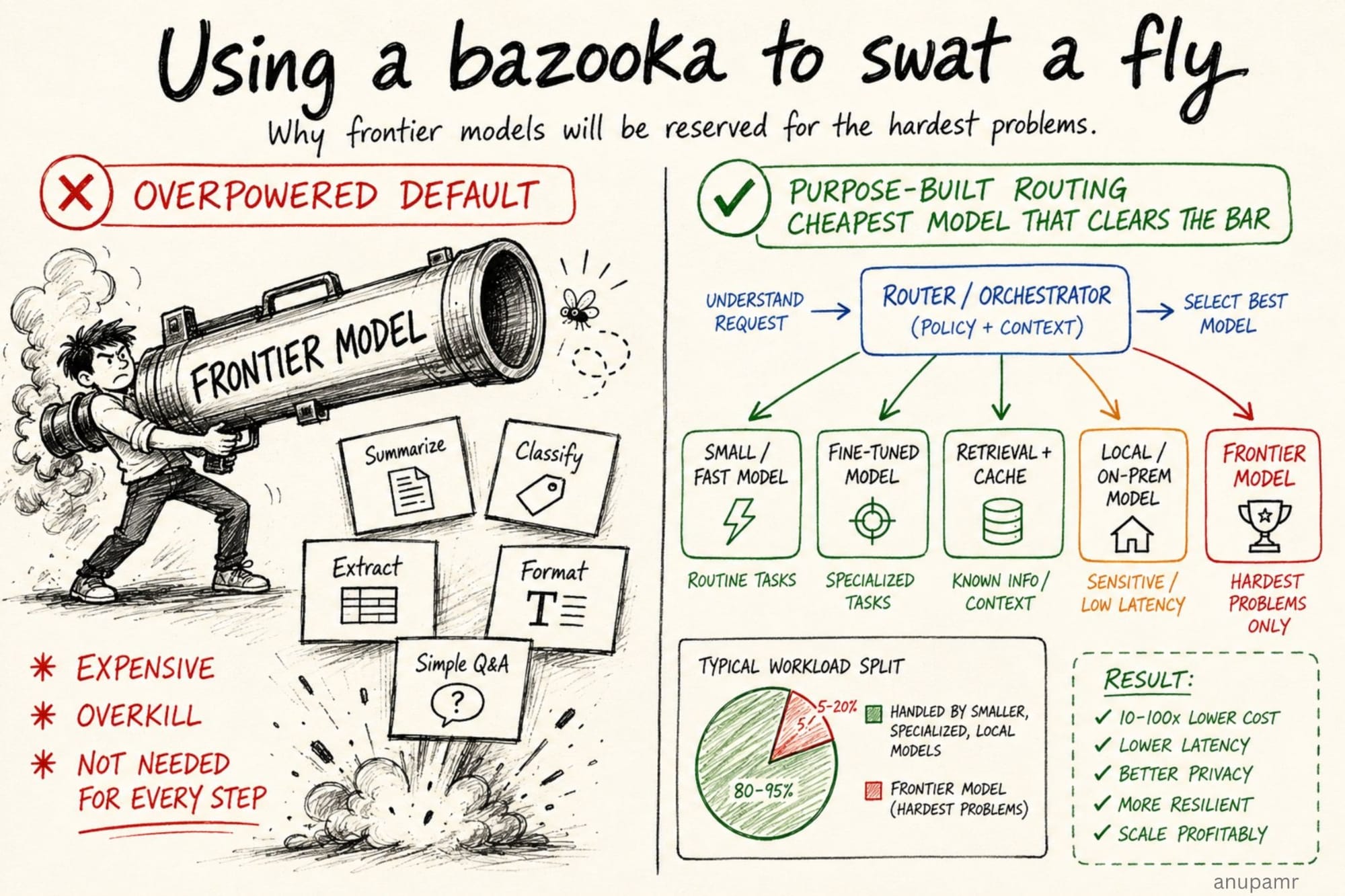

Between 2000 and 2025, global internet traffic exploded as video, mobile, and cloud reshaped life and business. Traffic grew roughly 7,000 times, from ~75 PB/month to ~522,000 PB/month. Essentially all of it moves across routers and switches, and Cisco, the pioneer of networking infrastructure, owned that layer. Yet over the same window, Cisco's revenue grew from ~$19 billion to ~$54 billion, a 2.8x increase.

Read that again. The traffic on the infrastructure grew 7000 fold. The revenue of the dominant infrastructure company grew 2.8 times. This disparity arose primarily from massive leaps in networking technology that drove extreme price deflation per bit, hyperscalers building their own custom infrastructure, and intensifying competition from white-box switches and software-defined networking. Importantly, Cisco was not one of the casualties. It was one of the great survivors of the early internet infrastructure cycle.

The most prized researchers of the late 90s cycle sat in the great labs at the foundational layer of that era - networking, hardware, and systems software - doing truly world-class science that still underpins the internet you are using now. Bell Labs, IBM research and AT&T Labs were among them, and I had a front-row seat to the density of talent and world-changing innovation happening there. But they struggled to convert path-breaking research into durable, value-capturing businesses. The research-richest companies were among the hardest hit in the bust. Bell Labs' parent, Lucent Technologies, was a defining casualty of the 2000 bust, with $250 billion in market cap erased in under three years. The research labs survived, but in much diminished form.

The point is that being essential to a technology is not the same as capturing its economics.

Volume going up is not the same as your revenue going up, and your revenue going up is not the same as your margins or stock price going up. Revenues and margins going up rapidly is not the same as durability and predictability.

Google shows the alternative path. Its usage was growing rapidly in 1999. I remember my entire lab at IIT Delhi switching to it practically overnight in early 1999, as it displaced AltaVista, Lycos and Yahoo as the entry point to the internet for us. Many companies were going public around that time on pure promise, and most are forgotten now. Google stayed private through the euphoria, launched AdWords in 2000, built it into one of the most profitable and predictable business models in tech, and had a generational run after its IPO during a tough 2004 market.

Different times, different scales. But that is the path today's frontier labs should take: IPO after predictability.

The bull case argues for staying private

The strongest argument for the labs runs differently from being primarily a provider of frontier inference or coding harnesses. It is that they use today's position to own higher layers of the stack: workflows, agents, enterprise control planes, developer ecosystems, digital labor, sovereign and defense applications, and perhaps entirely new interfaces between humans and computers.

They are already on that journey. The smartest people in tech run these companies, and I would not bet against their ability to escape raw inference economics for more durable business models.

But that is exactly the case for staying private, not the case for listing now.

Those transitions require experimentation, pricing changes, product pivots, conflict with partners and customers, margin volatility, and several false starts. Public markets are not built to patiently underwrite that kind of fluidity at trillion-dollar expectations.

Employees would welcome liquidity. Investors would welcome DPI. A successful IPO would likely be cheered by most. The capital requirements may already be testing the edges of what private markets can support, though recent rounds suggest those edges are still moving. The question is whether taking additional short-term pain today improves the odds of building a much more consequential company tomorrow.

There is also the question of whether a research-first culture has the culture-market fit required to run a true enterprise solutions business, if that is where the model ultimately points. That is a very different organism from a research lab, and the gap is not closed by talent alone.

I also think the frontier labs are charting the path to genuinely large societal advancements: compressing the timeline on scientific discovery, on drug and materials research, on hard problems in public health that have resisted brute-force human effort for decades, and potentially towards degrees of AGI over time.

That is the real reason to care how and when these companies go public. The breakthroughs depend on long, nonlinear, failure-strewn work, and you do not want to drop that kind of work into an environment that reprices it every day.

Final word

Inference demand is real, enormous, and growing. The revenue trajectories are explosive. The labs are extraordinary companies, potentially among the most important of our times. Given recent trajectories and current sentiment, they'd likely see exceptional IPO demand, especially if the market holds.

The trouble is timing. The labs are lining up to go public while the value-capture model is still being shaped, and public markets, with their reflexivity, impatience and quarterly referenda, are the wrong place to finish that work. The better path is to go public once revenue quality, margin durability, and market-share dynamics have achieved real predictability.

Raise the money in private, harden the business model, protect the mission, and let the public market price a business instead of a promise.

I write about where Enterprise AI value actually accrues, across foundation models, infrastructure, workflows, and vertical applications. Subscribe to receive future notes.