The Complexity Alpha

Why the next great Enterprise AI companies look too hard, too slow, or too messy before they look inevitable

A consensus is forming in Enterprise AI: that the action is mostly at the obvious places. Foundation model labs raising at mythical valuations. Infrastructure plays riding the GPU buildout. AI-native tools landing with individuals and expanding from there. These are real categories with real winners. The point of this piece isn't that they're wrong, but that they aren't the only path to scale outcomes, and a different and under-appreciated path runs through complexity.

Complex Enterprise AI companies are systematically under-appreciated at present. They attract lower attention than the underlying opportunity deserves till their scaling cadence becomes undeniable.

I call this the Complexity Alpha. It's where some of the most interesting Enterprise AI outcomes of the coming decade will be built.

The three crowded patterns

Most capital in Enterprise AI today is chasing three well-identified patterns: foundation model labs, infrastructure derivatives once they become obvious, and high-growth AI-native applications capturing individual workflows through bottom-up adoption. These are legitimate paths with legitimate winners, and most visible mega-cap AI companies today fall in these three categories.

The challenge for new investments at today's consensus AI valuations is not that the patterns are wrong. It is that they are well-discovered already. When the playbook is widely understood, valuations start to reflect best-case future execution, and there's little margin if growth turns out merely good rather than superlative.

Then there is the ephemeral nature of the crown in a space moving at lightning speed. Many of these positions are or will be exposed to head-on hits: e.g. simpler application categories that grow rapidly today by virtue of their simplicity get commoditized by the next model release. Infrastructure layers that get absorbed by hyperscalers extending their stacks.

There are categories that become hot quickly around a moment in the AI cycle which can lose definition just as fast when the cycle moves on - e.g. pure-play vector databases in 2023, RAG applications in 2024, or writing assistants back in 2022.

Hypergrowth in ultra-competitive AI segments also carries a flavor-of-the-season quality — hot today, forgotten tomorrow. Even the most preeminent AI companies are not immune to this. Just over the last year, the frontier model crown has traded heads every quarter. With Claude reigning supreme today with its usage being worn as a badge of pride by individuals and companies alike, it is easy to forget the brief near-crowning of Gemini in late 2025, Llama’s rise before that, Grok’s run at it, and the belief in OpenAI’s invincibility that had no dissenters till a few months back. And much of the enterprise demand is brand-agnostic by design. Programmatic usage flows to the cheapest model that clears the bar for the task, and re-routes the moment a cheaper one does.

Many of today's "inevitable" bets will turn out to be wrong.

The momentum playbook works because a few power-law winners absorb the losses, and the best momentum investors construct portfolios around this math. Many others are playing the same game without the same construct: effectively bearing early-stage risk priced at generational-company valuations, with no margin if the consensus is wrong.

Complexity alpha is a different lane. The companies are harder to evaluate, the early curves are non-linear, and their early valuations and progression can reflect that opacity. Yet, the terminal outcomes can be very large.

What we mean by complexity

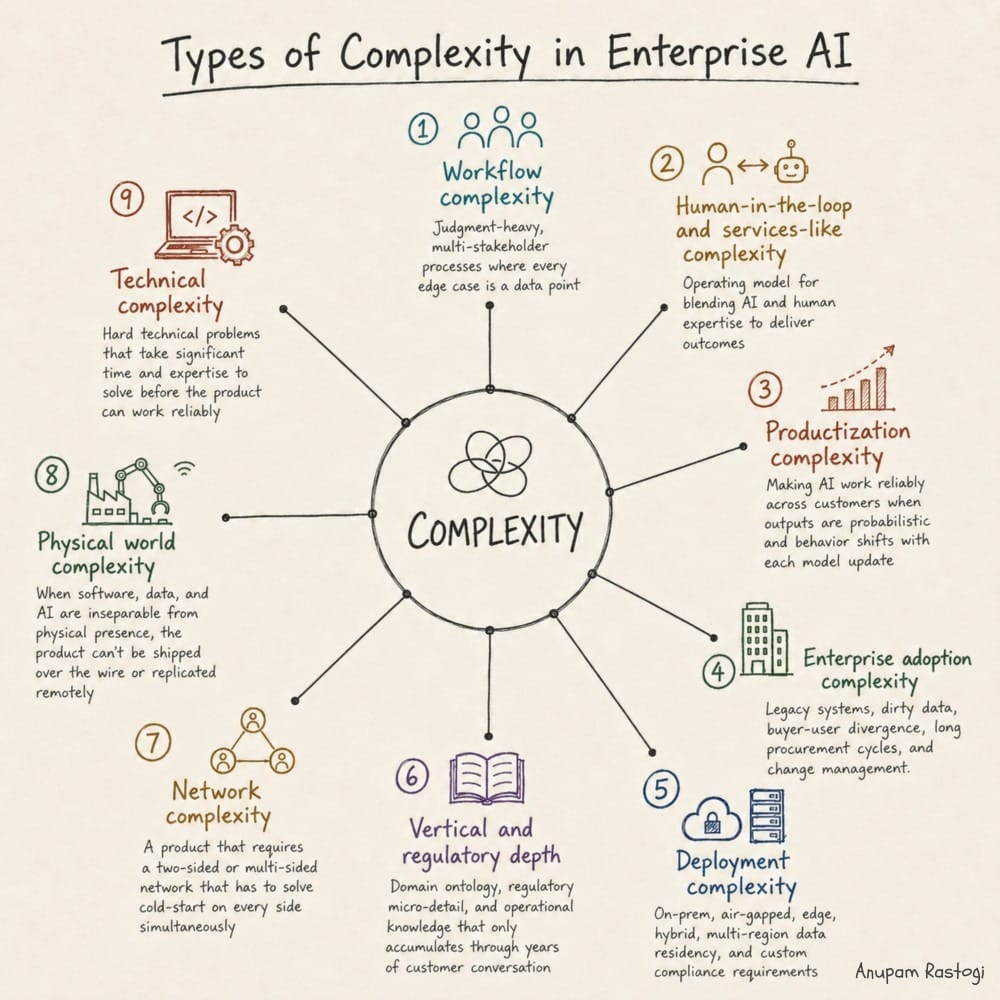

Complexity isn't one thing. The most interesting Enterprise AI companies tackle it across several distinct dimensions at once.

As AI makes the easy parts of enterprise software trivially easy, it raises the stakes on everything else. A simple voice agent for customer service can now be spun up in hours. One that draws on live enterprise and industry context, handles high-stakes conversations naturally across the full range of what customers actually ask, and does it reliably in production — that requires stacking several distinct complexity types at once.

Here are some types of complexity that deeper Enterprise AI companies solve for:

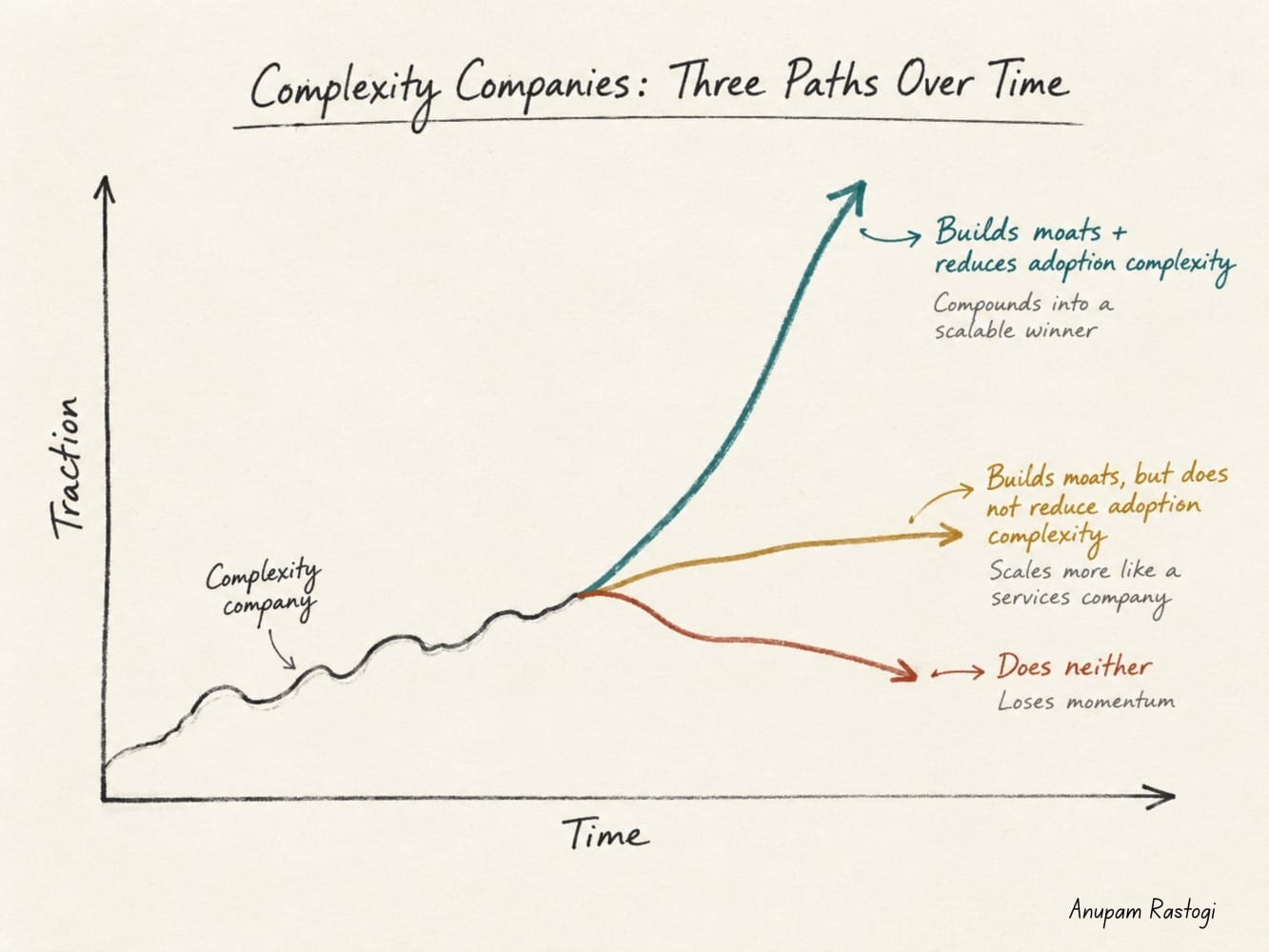

Complexity creates two opposing forces on the building company. Early on it makes these businesses harder to build, harder to fund, and harder to evaluate. That's what often makes them pre-consensus: they can look difficult to scale, or simply too opaque to underwrite before significant traction arrives and scaling velocity improves. The comparison to simpler AI categories doesn't help - some are going from 0 to $100M ARR in months, resetting the market's intuition for what a good early trajectory looks like. Against that benchmark, a complexity-heavy company in its first couple of years can look like it's barely moving.

On the other hand, the same complexity-related concerns that generate initial friction and skepticism are what can also build the moat.

The complexity stack, once worked through, can make the company nearly unassailable later.

The opportunity that sits in that gap, between early skepticism and eventual recognition, is the Complexity Alpha.

Complexity now vs then

The early SaaS and Cloud era rewarded simplicity. Many eventual winners started with clean adoption wedges and legible narratives, then compounded into broader platforms and deeper moats: Salesforce, Hubspot, Atlassian, Shopify, Workday were all in fairly legible categories with rapid early scaling, and many eventually surprised further on the upside by expanding markets.

Yet even in the SaaS/Cloud era, the largest outcomes weren't always the fastest-scaling simplicity winners. Veeva quietly built a $25B+ life-sciences company on just $4M of venture capital and converted vertical/regulatory mess into a compounding moat. ServiceNow got to $130B by working through workflow and adoption complexity in a category many viewed as backoffice plumbing. Datadog worked through data normalization and tremendous integration complexity to create what’s now an ‘obvious’ $75B business. Palantir spent fifteen years being mistaken for a hard-to-scale services business. The Complexity Alpha pattern worked then. It just wasn't the dominant narrative, because the simplicity playbook was producing faster, easier wins.

However, complexity isn't just a preference in this cycle. The new defensible surface lives in everything the model can't do alone - and that often involves complexity. An entire generation of investors trained their instincts in the SaaS environment, and the reflex to read simplicity as scalability still shapes how Enterprise AI companies get evaluated today.

Which complexity actually compounds

Complexity and moat aren't synonyms, though. Hard to build today doesn't automatically translate to hard to compete with tomorrow.

The most important question for any complexity-alpha bet is whether the complexity being absorbed in the early years is substrate resilient: complexity that remains hard to replicate as the underlying horizontal substrate technologies (foundation models today, but also quantum systems, world models, physical-AI stacks, and future technologies as they mature) keep improving.

Fragile complexity looks like elaborate prompt engineering, custom evals, fine-tuned model wrappers, clever orchestration to make today's frontier models work reliably for a particular domain. Two years of engineering investment here can potentially be replicated by a competitor in two months on a stronger base model. The pre-LLM NLP startup graveyard is littered with products that had real technical complexity, real customers, but no durable moat when the underlying capability commoditized. The complexity was real; the moat was an illusion.

Durable complexity is grounded in things horizontal technologies can't generate on their own. Proprietary closed-loop operational data that only accumulates by being deployed inside the customer's actual environment over time. Integration depth into legacy systems that no foundation model provider wants to sell into. Deployment footprint in on-prem and air-gapped environments where horizontal players have no interest in operating. Vertical ontology and regulatory knowledge measured in years of customer conversations. Physical-world presence that can't be replicated remotely. Trust capital and audit trails earned in regulated environments where switching cost is measured in compliance review cycles. Distribution into fragmented buyer markets that are individually small and collectively huge.

Robotics, physical AI, novel hardware, advanced materials, and applied quantum often sit closer to the extreme end of this spectrum. They combine workflow, productization, deployment, and physical-world complexity by construction. As AI capability turns increasingly into a substrate for physical action and scientific discovery, deep-tech enterprise companies are likely to be among the largest beneficiaries, yet their underwriting remains deeply uneven at the early stage — overpriced in select pockets driven by founder persona or ‘obviously large’ segments, but more often under-appreciated because the complexity is hard to price.

The discipline at the early stage is to underwrite the kind of complexity, not merely its presence.

A vertical AI company whose pitch is "we made the model work for X" is often riding a capability gap or execution alpha rather than building complexity alpha. A vertical AI company whose pitch is "we sit inside the customer's operations, accumulate a data and trust position no horizontal player can replicate, and the AI is one component of a deeper system of action" is the bet worth making. These two might read similarly in an early deck, but behave very differently over five years.

Best of both worlds: builder complexity, simpler adoption

Here is a critical point for investors and builders: complexity has two faces. There's the complexity the builder absorbs, which should compound into a moat, and there's the complexity the adopter faces, which determines how fast the company can grow.

The ideal complexity-alpha company progressively widens the gap between the two.

In year one, both are high. The product is hard to build and hard to adopt, deployment cycles are long, every customer is a custom engagement, integrations are bespoke. The team is doing services-grade work because no one else can.

By year three, the builder-side complexity has deepened into moats (more data, more integrations, more trust capital, more regulatory coverage, more vertical-specific ontology) while the adopter-side complexity has shrunk. Implementations that required extensive forward deployed engineering time now run through self-serve connectors. The first customer in a new vertical took a year of co-design; the tenth customer in that vertical takes a month. The same accumulated complexity that locks competitors out also gets progressively packaged into something customers can actually consume.

This is the best of both worlds: a deepening moat on one side, an accelerating growth rate on the other. It's the difference between a complex company that compounds into a venture-scale outcome and a complex company that plateaus as a bespoke services business. This arc is what to look for. Companies that absorb complexity without ever reducing the adoption tax tend to top out smaller than the moat would suggest.

The challenge is that the Complexity Alpha arc is almost invisible from the outside until it's well underway. That's precisely why the market often underweights these companies in the early years.

Why the market under-appreciates complexity companies early

Consider two companies. Company A posts a triumphant year with a quick 0->1 followed by 10x growth, but then decelerates, and runs a leaky bucket with 70% gross retention as the easy logos churn off or foundation models move into the space. Company B starts off slow as it solves for complexity, then grows at a steady 3x, then 2x, reaching public company scale in 7-10 years with 120% net revenue retention and 95% gross retention. By then, Company A has a smaller and lower-quality book.

Company B is the better business, but Company A is the natural center of investor attention in the initial years amidst its momentum. Of course, there is also the ideal company C that grows 10x in the first year, retains superlative growth rate and momentum, and builds strong retention over time. Those are the truly rare and valuable consensus investments.

Many good early investors know the Company A vs B dynamic well, but complexity companies still find it hard to raise their early rounds unless they are in a hot space with a storied founder. Three structural reasons:

- Fund mechanics: In the near term, early-stage investors get evaluated on externally visible signals of success such as later-stage rounds and legible portfolio momentum. Complex companies have non-linear early curves; the first few years often look unremarkable and then suddenly they don't. Incentives penalize this, and it naturally pulls many investors toward stories that produce rapid markups.

- Structural division of labor between fund types: Large multi-stage platforms operate with explicit constraints: target position sizes that can't be deployed efficiently into early complexity companies, partner time that has to be allocated against fund-returner potential at scale, return thresholds calibrated against very large fund sizes. Waiting for scalability to become legible before underwriting is rational.

- Discerning "this is complex now, but scalable and durable later" from "this is just slow" requires conviction based on technical depth, operator networks, and domain perspective. This can be time-consuming hard work - and the gravity in a highly noisy market like this one pulls constantly in other directions.

What this means for founders and investors

The thesis above is good news with caveats, and getting the caveats right is most of the job. Here are some of my learnings for those building complexity alpha businesses and those backing them:

Have a dominant moat strategy from day zero. What is your compounding moat going to be: data, metadata, ontology, deployment footprint, integration depth, regulatory position, distribution, trust capital? Each implies a different early-stage roadmap, different early customers, different data architecture, different terms with first design partners. Founders who treat moat strategy as something to figure out later often end up with neither the easy growth of a legible category nor the durable position of a complexity-alpha company. Pick the moat early. Architect the first few years around accumulating it.

Be clear about the complexity types you're stacking. Workflow, HITL, productization, technical, integration, deployment, vertical depth, physical world. One alone is often just a feature. Two or more, compounding together, start building something genuinely hard to replicate.

Be capital-efficient by design. Complexity companies can't count on rapid, high valuation follow-on rounds in the early days. Plan capital reserves for stretches where the chart looks unimpressive followed by inflections that take time to translate into ARR. Less burn means more optionality.

Engineer the adoption-complexity arc deliberately. Builder-side complexity should compound into moats over time. Adopter-side complexity should shrink. Watch for deployment-cycle compression, templated integrations replacing custom ones, and improving expansion economics as cohorts mature. If those numbers aren't moving in the right direction by year three, the moat may be real but the business is not on a venture-scale path yet.

Many of the companies that define Enterprise AI over the next decade are being built right now in spaces the market has decided are too complex for now.

Complexity alpha is a structural bet that the market overpays for legibility, and that the gap is widest in cycles like the current one when the legible categories are flooded with capital. Ultimately, Enterprise AI will reward companies that absorb complexity so customers don’t have to. Investors should treat it as one part of an early-stage portfolio rather than a contrarian pose or a universal strategy, and allocate with discipline against the gap.

I predict that a majority of the top fifty Enterprise AI companies by revenues a decade from now, excluding large horizontal platforms, will be ones currently invisible in the AI narrative - pre-consensus compounders hiding in plain sight. They will share most of the following: they are solving multi-faceted complexity in domains today's hype investors find too messy; they are building moats that get stronger as foundation models improve; and they have engineered the adoption-complexity arc deliberately, so what looks like a slow start becomes an accelerating curve.

These companies don't look like the headline names of today. They are harder to underwrite, and slower to show their hand. That’s where Complexity Alpha lives.